In 1981 when the tightening started, unemployment was about 8.5, rose close to 11 in 82 and dropped to 8+ in 83 then started going down slowly.

I honestly don’t know what to expect, this situation with rates and QT is something new.

In 1981 when the tightening started, unemployment was about 8.5, rose close to 11 in 82 and dropped to 8+ in 83 then started going down slowly.

I honestly don’t know what to expect, this situation with rates and QT is something new.

The wildcard is all the baby boomers retiring. So unemployment may not hit highs we normally would because the workforce is shrinking.

Those retiring baby boomers might cause a stock market sell off.

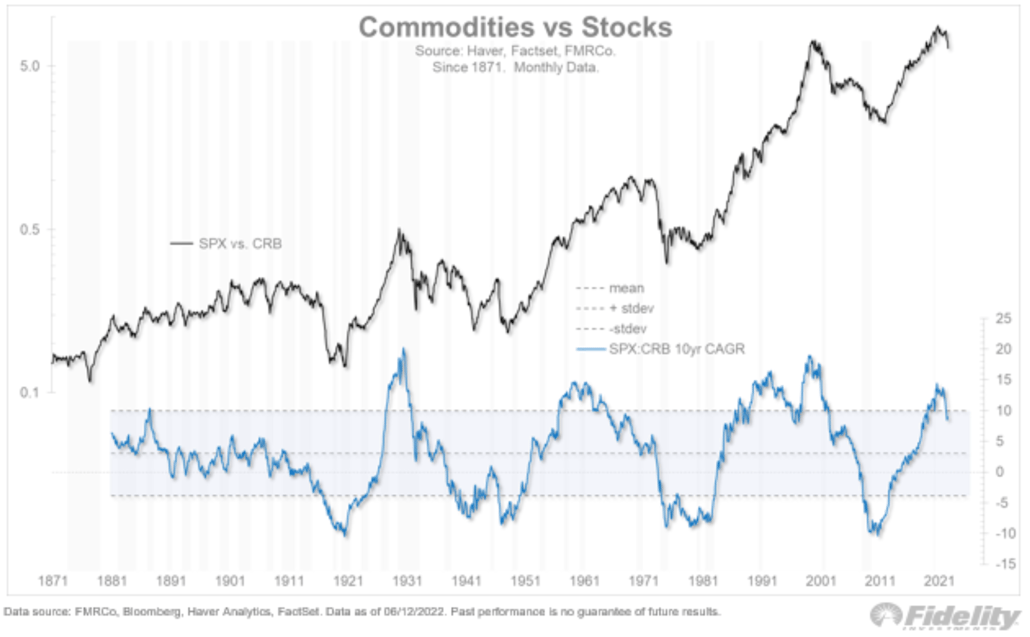

Chart of the Day

With hopefully deflationary Fed-driven asset destruction underway, the super-cycle of commodities relative to stocks may have plenty of room to run higher.

The chart below reflects the CRB Commodity Index versus stocks since 1871 (black line), plus the compound annual growth rate (CAGR) of that ratio (blue line). As shown, commodities historically undergo upswings that can span decades when they’ve surpassed a previous high.

On Tuesday’s Daily Briefing, Tony Greer joined Maggie Lake to shed light on the volatility in the natural gas market, discuss the implications of longer-term supply constraints in the energy market, and share some actionable trades that he’s monitoring.

If you know Tony, you know he’s long the Great Rotation, so it should come as no surprise that he’s bearish Big Tech amid our rising-rate environment. But, according to Tony, the steep sell-off in equities is causing a broad drag across asset classes in the short-term.

Watch Now: Keep Calm and Manage the Volatility

Money Thread ![]()

When legendary energy trader Pierre Andurand speaks, we listen. And when he tweets pure alpha that runs contrary to popular political and economic opinions, we put it in this newsletter.

The kicker?

For more from Pierre, don’t miss his recent interview with Real Vision co-founder and CEO Raoul Pal on how a secular super-cycle in commodities could spark a global financial crisis, and how that will accelerate the drive to invest in a more sustainable, “net zero” future.

What do you guys think about Meta (Facebook) last I checked it was at 160. That’s the lowest in a long time. Same with carnival cruise (CCL) selling at $8 earlier in the day.

I’m not making a call here — just linking to some bear markets history…

https://twitter.com/AlmanacTrader/status/1537539892770754560?s=20&t=uuNO9LM6rPzuQlIaDMJcaQ

Interesting Moodys analysis

https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_1332395

Here’s what works for me. I hope it helps a bit…

(1) I would say No — don’t time the market unless you have a well-thought-out plan on when to get out, when to get back in, how much to buy & sell, and you’ve tested it on the last several bear markets.

(1b) If you contribute to your 401K every month, then when the market is down you’re buying more shares for your money, a smart move.

(2) I stick with an S&P 500 index fund. Yes, at any point in time there will always be something that’s beating it: bonds or gold or oil, smallcap, foreign, etc., but the S&P 500’s very-long-term growth rate is a solid ~10%, and sticking with the S&P 500 means (a) you won’t have to worry about what to switch into & when to do it (b) the news will always let you know how you’re doing (c) fees will be rock-bottom so you’ll keep more (see 6, below re: fees).

(2b) S&P 500 — Warren Buffet has instructed his executors to keep his wife’s portfolio 90% S&P 500 and 10% short-term bonds — he’s said it’ll beat most investment managers. Buffet: “My advice to the trustee couldn’t be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (Buffet suggests Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors — whether pension funds, institutions or individuals — who employ high-fee managers.”

(3) ALWAYS grab any employer 401K match — if they match 3% or 6% — take it ALL — it’s an IMMEDIATE 100% return!! Literally Free Money. An absolute no-brainer.

(3b) Start early in your career with the goal of raising your 401K contribution as much as you can as soon as you can. For 2022, you can do $20,500 max. Workers who are 50 and older can make an additional $6,500 in catch-up contributions. Employer match adds to that. Do the math with XL, one row per year of your career, assume a simple annual return of 8% or 9%, and you’ll see that starting as early & as large as possible makes a really BIG difference in ending values.

(4) Do Roths if you think tax rates will be higher in the future (I think so).

(5) If you’re very close to retirement or in retirement then keep a couple/three years needed withdrawals in short-term investments like cash, CDs, short-term bonds — with this short-term money on hand you won’t have to sell cheap at the bottom of a bear market to meet your expenses. There are numerous plans for how to replenish cash — see James Cloonan’s “Investing at Level 3” book for one way to do it (brief recap at bottom).

(6) Fees matter. A 1% fee for 20 years = 0.99^20 = 82% so -18% lost to fees. A 0.05% fee (like several S&P 500 funds & ETFs) for 20 years = 0.9995^20 = 99% so only -1% lost to fees — BIG difference. Watch out for custodian fees, too — that’s the fee charged by your 401K manager, the folks who send you your statements — if you think their fees are high show the math to your employer and ask them to get a thriftier custodian.

— Best, Steve

The Level3 withdrawal approach incorporates two types of assets. the first is equities: A high allocation to them is maintained to allow a portfolio to grow at a rate faster than inflation. the second is defensive: Defensive assets are those that are safe from the standpoint of a drop in actual value. such assets include short-term treasuries, CDs, & money market funds. the defensive allocation is established during the four-year period leading up to retirement. each year that the S&P 500 index starts within 5% of its previous high, one year’s worth of expected withdrawals is shifted from equity to defensive. once retired, withdrawals are taken from the equity allocation if the market is within 5% of its previous highs. If the S&P 500 is more than 5% below its highs, withdrawals are taken from the defensive portion. (see AAII.com for more Level 3 info)

I am really fortunate. My company (UKG) has a 45% 401(k) match…uncapped. I make damn sure I max out every year. I’m also old enough to contribute to the catch up plan, which I try to max out as well.

45% ??? Wow !!! Lucky  Dog!

Dog!

You should see the rest of our benefits package. I wake up every day and say to myself, “don’t get fired today”.

Got a name for this one yet ? We did the Great Recession in 2007-2009, so that one is taken.

The Roosky Recession, Great Recession 2, Greater

Recession, ???

The Brandon Recession

“I did that” Recession

Walked right into that one

Yep ! Since the QE from the Great Recession never

got unwound, I’m thinking there will be some linkage

in the naming.

A @WSJ chart illustrating the downward revision in US growth projections for the current quarter.

These downward growth revisions have been accompanied by an upward revision in inflation.

#economy #EconTwitter #inflation #growth https://twitter.com/elerianm/status/1537751477707489281/photo/1

Warren Buffet’s 98-year old sidekick Charlie Munger is very smart, IMO. He has a lot of sayings worth remembering & here’s one of them —

“There are three ways a smart person can go broke: Liquor, Ladies, & Leverage.”

In the crypto space, I think a lot of leverage is being unwound, some of it forced liquidation. That’s gonna have to run it’s course. Liquidations in China (Evergrande, etc.) will spill over into Bitcoin. Note that Bitcoin trades online 24x7x365, not on exchanges with limited hours. Here’s a live Bitcoin quote — https://www.cnbc.com/quotes/BTC.CM=

Unrelated, here’s another favorite Munger saying — “Show me the incentives, I’ll show you the outcome.”

I’ve never invested in crypto, I don’t really understand it and so always thought it was a bit of a roulette wheel, but damn bitcoin is falling like a rock.

Wokeresession

Does anyone really understand Bitcoin mining?

© 1999-2025 CoogFans.com