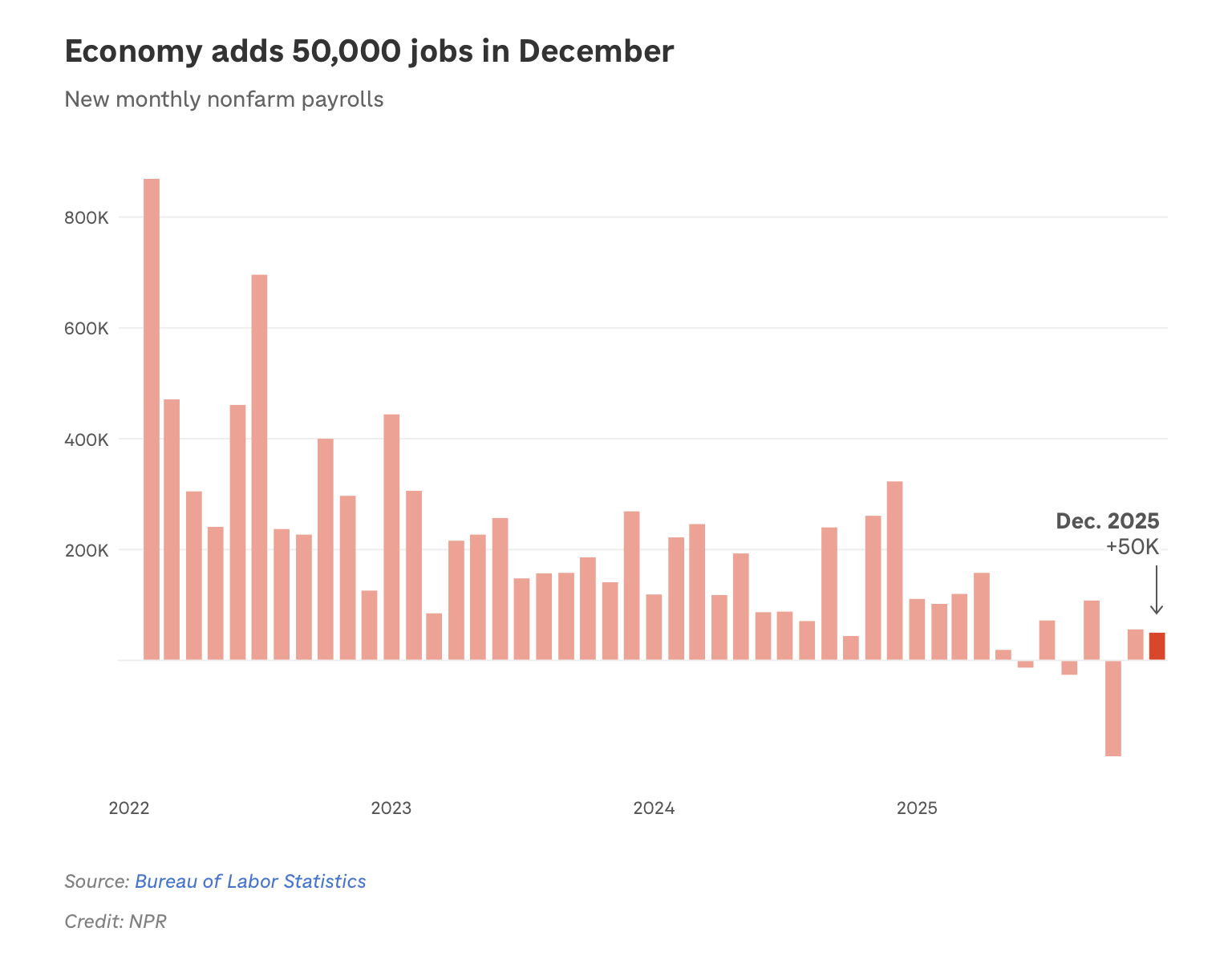

The market is not the economy. No question stock market last year performed

very well despite the on again , off again tariff policy. But there are serious cracks

here. The graph doesn’t lie.

Wall Street isn’t Main Street. The last guy learned that.

Never mind that federal job losses are still job losses to the people that lost them. They are now competing with others looking for work, likely with a more impressive resume to some.

Job losses are job losses. Period.

2 Likes

Duh! It is, however, what the money people forecast the next 6 months

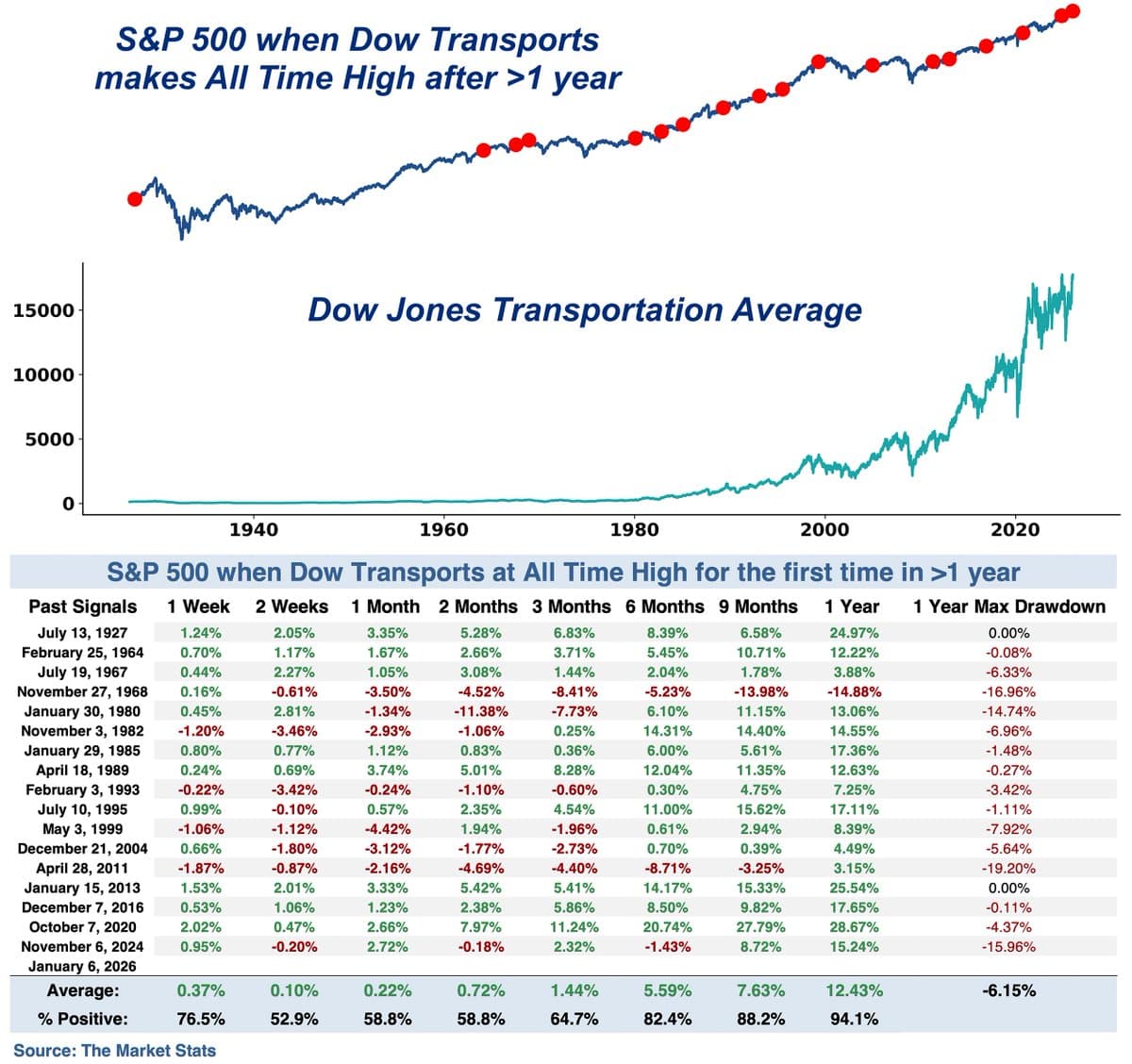

Based on this week’s moves—both the Dow Industrials and Transports hitting record highs together on Tuesday—we got a classic Dow Theory buy signal. It’s the first one in over a year, confirming the bull trend’s still intact — Grok

https://x.com/stevokeefe/status/2009960614035399027

.

.

.

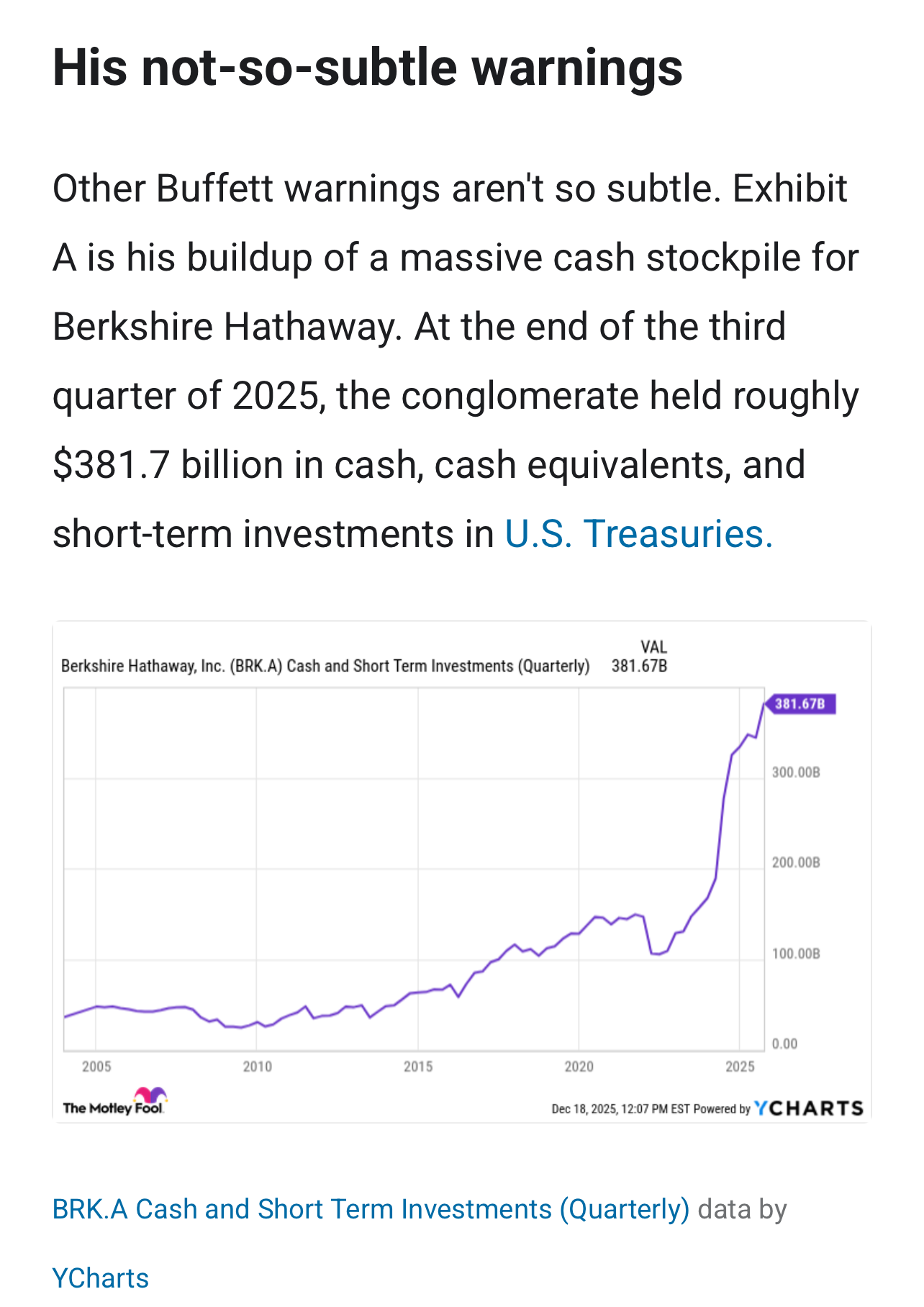

Exhibit A, Warren Buffet. This money person

thinks the market is overvalued. P/e ratios are

very high.

Ever hear of pump and dump ?

But if you feel equities are the place to be right now, double down on your bets.

interesting thread, first time looking at it; always assumed it had something to do with star wars.

anyone new to markets, i highly recommend getting lance roberts - realinvestmentadvice.com weekly; he’s very good. imo, he’s really just a chartist that puts out lots and lots of info to support his charting but he called the 2008 meltdown in dec 2007 and was ahead of the covid drop a month early.

1 Like

1 Like

See much difference ?

TOTAL 2025 1,821,931.3 2,875,829.7 -1,053,898.3

TOTAL 2024 2,061,690.8 3,266,410.2 -1,204,719.4

TOTAL 2023 2,020,479.2 3,076,796.4 -1,056,317.2

TOTAL 2022 2,072,648.0 3,239,732.9 -1,167,084.9

TOTAL 2021 1,757,743.7 2,828,515.5 -1,070,771.8

https://www.census.gov/foreign-trade/balance/c0004.html#2025

1 Like

It’s getting harder and harder to distinguish American free markets and

capitalism from other systems. What are y’all’s thoughts on this proposal to

limit what credit card companies can charge ?

The other question is if the economy is doing so fine, why is this needed ?

It’s unclear if the president will attempt to enforce his proposed 10% cap through some kind of executive action, or if his goal is to pressure credit card issuers to slash their rates voluntarily. CBS News has reached out to the White House and some of the largest credit card issuers in the U.S. for comment.

10% rate for a credit card is crazy low and impossible.

That said, not sure if this pressure to lower or actually get to that number.

My thought is that the borrowers agreed to pay those interest rates when they used the cards and didn’t pay the money back. That’s a contract, and nobody forced them to do it. People with riskier credit profiles pay higher interest - that’s the way it works.

There are statutory limits on interest rates (usury laws), and Congress can take action to limit these further. In fact, Bernie Sanders proposed just such a cap last year, but there was no interest in pushing it forward.

https://www.congress.gov/bill/119th-congress/senate-bill/381

But credit card companies will just cancel cards and/or limit credit lines if there’s some hamfisted executive order that prohibits them from protecting themselves through interest rates. And part of the reason these rates are high is due to ongoing bank deregulation. This is just more hand-waving, imo.

1 Like

Not surprising.

It’s populism. Populism was a big part of what Donny ran on.

Same with the Democrats.

1 Like

It’s also curious when juxtaposed against the opposition to student loan forgiveness. The primary difference is that one encourages spending, while the other one encourages education.

Credit cards have a fascinating history if you’re into this kind of thing.

Brief History from Grok (take with a grain of salt)

- The Diners Club card launched in 1950 in New York City as the first multipurpose charge card, allowing users to pay for meals at 27 restaurants, mostly in the NYC area. American Express followed in 1958 with its own card. BankAmericard, predecessor to Visa, also debuted in 1958, introducing revolving credit in 1959.

- Charge cards in 1950 required full monthly payments.

- High inflation in the 1970s pushed borrowing costs above state usury caps, limiting bank profits. A 1978 Supreme Court ruling allowed national banks to apply home-state interest rates nationwide. South Dakota repealed its usury laws in 1980 to attract jobs, leading Citibank to relocate credit card operations there in 1981.

- Then credit access was greatly expanded because losses from poor credits was covered by the income from higher interest rates.

If we go back to lower rates, I expect credit access to shrink.

(I don’t have a dog / politician in this fight.)

Good historical background.

I susupect if the CC companies agree to lower rates or forced into lower rates,

they will be less profitable and possibly have cutbacks and limit credit to folks who are at high risk. Not sure how profitable they are, but if cut to 17%, 15%, or 10%, that impacts their bottom line. So, as you say, it could lead to a contraction in consumer spending overall - an unintended consequence. For those with high monthly balances, it’s great. Like getting a personal tax break or subsidy. Apparently about 46% of folks carry a monthly balance.

AI Overview

The average U.S. credit card balance hovers aroundemphasized text

$6,000 to $7,000, with recent data from late 2025 showing figures like $6,618 (Experian, Experian and Experian WalletHub, WalletHub and WalletHub) or $6,735 (Experian, Experian and Experian) per person, though some sources show averages around $5,600 to $6,200, with Gen X often carrying the most debt and balances varying significantly by credit score, age, and state.

2 Likes

Another thing that will happen is that the rewards programs will get cut back.

2 Likes

A mortgage backed by the home as collateral is ~6% right now and someone is suggesting a credit card (with no collateral) should be 10%?

It’s absurd. But maybe that’s intentional, idk.

1 Like

!!??!!

1 Like