JetBlue (JBLU) is navigating a challenging financial period in early 2026, marked by a widening Q1 net loss of ($319) million due to rising fuel costs and operational disruptions. While revenue grew by 4.7% to ($2.24) billion, the airline is cutting capacity for 2026 to stabilize costs and targeting breakeven operating profitability. [1, 2, 3]

Here’s a couple of snippets where he shows how the Big 4 airlines would compete—

• The big airlines have a host of advantages over the little guys, and they exploit them. They have lots of slots at airports, ‘fortress hubs,’ and scale in credit card programs, as well as reciprocity with each other but not the little guys… For example, in a brief last year, airline analyst Bill McGee did a case study on how Southwest Airlines intentionally lost money for years on its routes in Hawaii to drive Hawaiian Airlines out of business. In most of Southwest’s domestic routes less than 250 miles, it charged at least $159. But in intra-island Hawaiian flights, its prices were $39, and it lost money on more than half of them. And these weren’t some introductory price, the money losing occurred for five years. Eventually Hawaiian Airlines bled out, and sold itself to Alaska Airlines.

• I heard a thesis from an investor… who tracked what happening in real-time. He did research and realized the big guys figured out they could make Spirit’s business model non-economic with a strategic pricing strategy. Here’s what he told me. Consumers of low fare airlines tend to book a few weeks before their trip. So a few weeks before a Spirit flight from, say, New York to Orlando, one or more of the big guys would radically discount their price on just 20 seats on a similar route. The discounts would come on a flight the same time as the Spirit flight, so a direct competitive choice. This move would pull 20 passengers from a Spirit plane that could carry 220 people, meaning the flight would lose 9% of its revenue. That pushed such a Spirit flight from being profitable to being in the red. Spirit could either respond by dropping prices on all 220 tickets, losing money that way. Or it could give up on those 20 passengers, and lose money that way. But because the big carriers were willing to strategically forfeit revenue on those 20 seats, it meant Spirit would stop making money.

Yep, and airlines have seemed to have had a hard time staying profitable

and in business in the competitive era. Braniff Airlines went belly up, Continental and United both went in and out of bankruptcy, and then merging (which I hated for Houston losing its hometown HQ airline) and of course Trumpp Airlines…probably many others. Seems to be a hard business to stay profitable in.

So I’m not sure I’m for or against airline mergers.

Fun fact, my parents were going to take our family to Hawaii for spring break 1982 via free standby travel my mom had from being an ex Braniff flight attendant (they called them Clipped Bees).

As a family we voted to change it to a 2 week trip and go over the summer.

A classic Warren Buffett story. After losing money on USAir preferred stock in the late ‘80s, he joked that he set up a 1-800 number he’d call whenever the urge to buy an airline hit him. He’d say, “My name is Warren and I’m an aeroholic,” and the person on the other end would talk him out of it.

He repeated some version of that line for years, right up until Berkshire bought big stakes in the major U.S. airlines in 2016—then sold them all in 2020 at a loss during the pandemic. The story still holds up as a warning about how capital-intensive and competitive the industry is.

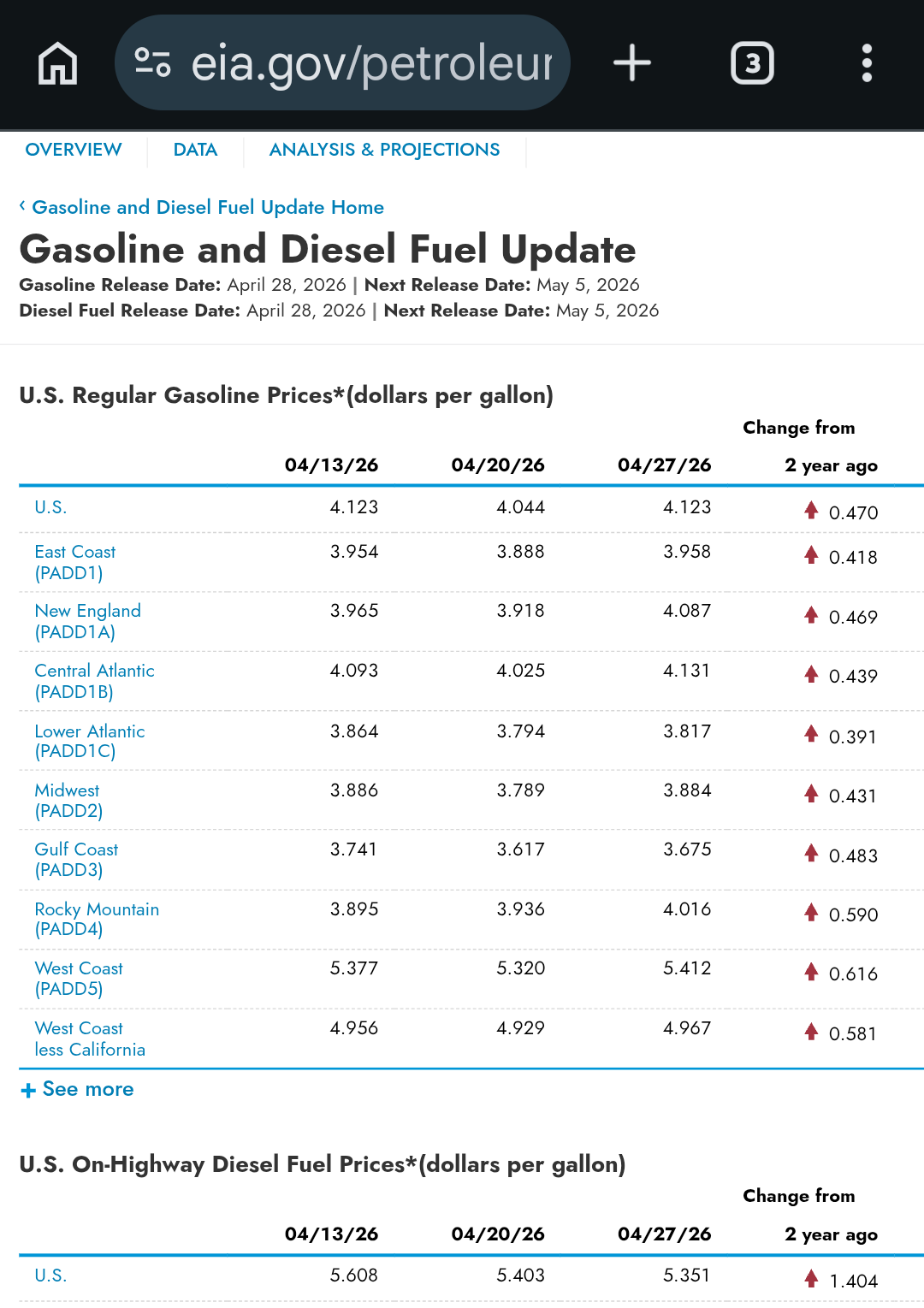

I think it was actually a bit higher a few weeks ago (like over $5.60), but we’re exporting more than our supply can handle, so this is going to remain a problem.

These massive exports are going to put us in a supply pinch if they continue. People may not realize it, but domestic oil production has declined fairly steadily over the last 6 months (though not by a huge amount), and the rig count has dropped by 37 from a year ago, which means there’s no production bump coming anytime soon. Companies are drilling longer laterals to maximize their financial returns, but they’re also drilling lower-tier acreage now, so the initial production rates are lower and the declines are quicker.

This isn’t a domestic oil production emergency, but what we’re seeing is that even at current prices, US producers can’t just produce appreciably more and aren’t ready to invest more, because their well break-even prices are higher than they’ve ever been.

I got stuck in Hawaii and extra 4 days when ATA shut down temporarily. They gave us vouchers good for two additional round trip tickets to Hawaii.

They shut down a month or so later.

They put us up at a so so hotel in Waikiki, but had to stay close to the hotel because we never knew when we were flying out, so it wasn’t a great extra 4 days.

There’s a pretty good chance that if JetBlue and Spirit had merged, then it would just be a much larger company declaring bankruptcy right now. Spirit’s debt was already crippling, and it’s not like JetBlue is so awash with free cash flow that they could manage that debt and the jet fuel squeeze.

The politicians out there trying to insist otherwise convinces me that this is what would have happened.

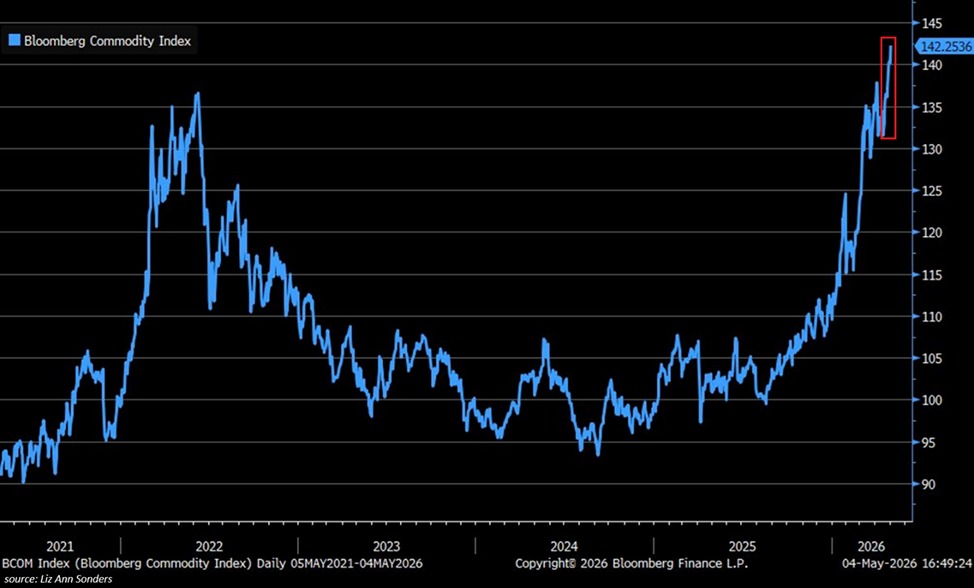

“The Bloomberg Commodity Index (BCOM) is a premier, diversified benchmark tracking 24 exchange-traded futures contracts on physical commodities, including energy, metals, and agriculture. It offers broad, liquid exposure, designed to prevent any single commodity or sector from dominating, with significant weightings in energy, precious metals, and agriculture.”