Another Jenga part comes out

Another Jenga piece coming out?

Another Jenga part comes out

Another Jenga piece coming out?

Published by Statista Research Department, Jun 29, 2023

Vacancy rates across the office real estate sector in the U.S. increased during the coronavirus pandemic. Before 2020, the quarterly vacancy rate was around 12 percent but as the pandemic unfolded, it climbed to above 15 percent. In the first quarter of 2023, about 16.1 percent of office space across the country was vacant. In some of the major U.S. markets, vacancies reached up to 30 percent. With a considerable part of the workforce working from home or following a hybrid working model, businesses are cautious when it comes to upscaling or renewing leases.

The COVID-19 pandemic has changed the way that companies operate, and working from home has become the new normal for many U.S. employees. The function of the office has evolved from the primary workplace to a space where employees collaborate, exchange ideas, and socialize. That has shifted occupiers’ attention toward spaces with modern designs that can accommodate the office of the future. Many businesses used the pandemic time to revisit their office guidelines, remodel or do a full or partial fit-out. With so much focus on quality, older buildings with poorer design or energy performance are likely to suffer lower demand, resulting in a two-speed market.

Simply put, if landlords do not have tenants, their income stream is disrupted, and they cannot service their debts. April 2023 data shows that several U.S. metros had a significantly high share of distressed office real estate debt. In Charlotte-Gastonia-Concord, NC-SC, more than one-third of the commercial mortgage-backed securities for offices were delinquent, in special servicing, or a combination of both. Nevertheless, offices had a lower delinquency rate compared to other commercial property types, such as lodging or retail properties.

Construction of a 33-story co-living apartment project in the Museum District has stopped, leaving the project, called X Houston, partially complete and dormant with no clear indication of when work will continue. X Houston was expected to be one of the city’s first co-living projects built from the ground up. Co-living is a form of roommate housing in which renters lease space by the bed, often with more affordable, flexible lease terms, while sharing common spaces.

(paywall, the crazy link may allow you by paywall)

Stanley Druckenmiller on the Fed’s historic blunder: "When rates were practically zero, every Tom, D!ck and Harry and Mary in the United States refinanced their mortgage, corporations extended. Unfortunately, we’ve had one entity that did not and that was US Treasury.

![]()

Carl Quintanilla

@carlquintanilla

](https://twitter.com/carlquintanilla)

·12h

worst recession. ever.

Quote

![]()

Liz Ann Sonders

@LizAnnSonders

·

12h

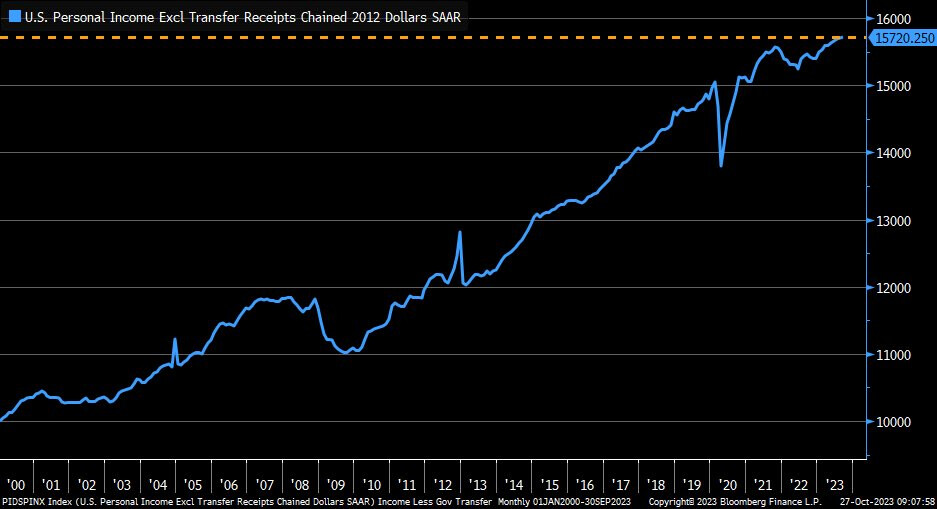

Real personal income excluding government transfer payments rose to new all-time high in September

You might want to adjust that graph for inflation and then see what it looks like. I seriously doubt that “real” personal income in the U.S. has risen very much, if at all, in the past 20 to 30 years.

Got another 12 months to find that recession. It may be around the corner, or it may be far away. Whether or not that graph is accurate, people are spending more and are looking for someone to blame, so showing them they earn more doesn’t matter in the real world.

Anytime you see the word “real” in an economic sense, it means it is adjusted for inflation.

Good point to make about “real”.

It’s an impressive graph…but…

in this graph the title has a blurb about “Chained 2012 Dollars SAAR”.

And I’m not clear what that even means and too lazy to dig into it. I’m guessing

2012 is maybe a baseline or something ?

That was my assumption. It’s using 2012 dollars.

When the government stops spending money you will.

Just as investors were finally catching on to the importance of following Treasury supply announcements, they were caught off-guard again yesterday by the early release of the government’s borrowing plans.

The past three months have made it clear just how important the supply of Treasuries is for financial markets. That’s not normal. The way it’s “supposed” to work, the economic data dictate where bond yields go next. Hence the importance of the monthly jobs report, ISM manufacturing, the inflation prints, etc. But that’s been upended since July 31.

That date was the last time Treasury released its quarterly debt issuance plans. Few investors were on the lookout for the release at the time. It was only after the details were published that markets went wait, what?! And that’s because Treasury not only had to increase its planned borrowing for the first time since Covid hit, but revealed it would look to raise $274 billion more than previously expected for the third quarter, because of the larger-than-expected federal deficit.

“All the current debates about budgets and interest costs, etc., stem from that announcement,” strategist Dan Greenhaus of Solus noted. The 10-year Treasury yield poked above 4% that week and would go on to jump a full point, to 5%, in the “rate shock” we’ve been experiencing in the months since.

Which brings us to now. Investors have certainly been on the lookout for Treasury’s quarterly supply updates. Their website indicated their full borrowing plans (“refunding,” as it’s technically called) would be released tomorrow, November 1. Plenty of market watchers have warned that this release could be more important than the Fed decision which is also tomorrow, or the payrolls report on Friday.

But at 3 p.m. yesterday, Treasury caught markets off-guard by putting out the blueprint of their intentions. “The Treasury Department apparently releases their data randomly,” wrote strategist Brian Reynolds of his eponymous research firm this morning. “We wish [they] would release an official data publication schedule well in advance…but it is what it is.”

So what did we learn? That, as Reynolds has correctly anticipated, the Treasury’s borrowing needs are now actually slightly less than previously planned this (fourth) quarter; $76 billion less, to be exact. Why? Because Treasury’s cash balance is already higher than expected at this point, and they’ll get additional revenue from delayed California tax payments next month, and corporate tax payments in December.

The knee-jerk reaction to this news, as expected, was lower bond yields. Not a huge move, mind you, but the report’s under-the-radar release no doubt played a role in that; plus, it took awhile for investors to fully digest the significance of their announcement last quarter, too. The 10-year Treasury yield this morning is around 4.85%, and markets may also be waiting for details in the “official” release tomorrow of Treasury’s exact intentions for issuance on the short versus long end of the curve.

But with this one big datapoint now effectively out of the way, it may well clear a path for lower bond yields in the months ahead. That will be especially true if the economic data slow, or the Fed is dovish. “Our most likely case is for bonds to rally down to the 4.24% area [by January] based on the decrease in borrowing,” Reynolds wrote this morning, “which would also benefit stocks.” (Although if the jobs report comes in super strong or the Fed is much more hawkish than expected, yields could go back above 5%, he cautions.)

None of this is to say that the country’s fiscal problems are solved. They will actually worsen as we go into the recession that still appears to be lurking around the corner. But a weak economy with high bond yields is much more dangerous than one with lower borrowing costs. At the very least, a significant drop in yields would be a welcome respite for consumers, businesses, and the U.S. government.

It behooves all to watch the complete interview. Beyond worrisome

Why did Jamie Dimon sell lots of shares?

Businesses beware: It’s about to get ugly.

WeWork, the real-estate company that cosplayed as a tech startup, filed for Chapter 11 bankruptcy this week. It’s not exactly a shocking resolution for WeWork, which first showed signs of its demise during a disastrous IPO attempt in 2019.

But one Wall Street veteran believes WeWork will be the first of many companies to succumb to a similar fate. In a recent note, New Constructs CEO David Trainer said hundreds of “zombie companies” — unprofitable businesses holding significant debt and burning through cash — will also file for bankruptcy, writes Insider’s Jennifer Sor.

Trainer’s concerns aren’t unfounded. More US companies filed for bankruptcy in the first eight months of the year than the total number of bankruptcy filings in 2021 and 2022, according to data from S&P Global.

Defaults on corporate debt have also been on the rise globally, per another S&P Global report. Bank of America estimates we’ll see $46 billion in distressed debt next year.

Rising interest rates have been a key culprit.

After years of a near-zero rate environment, getting money became a lot more expensive. That type of change throws quite a wrench in your plans if your business strategy amounts to burning cash while you figure things out.

S&P Global

WeWork kicking off a hypothetical bankruptcy boon is fitting.

The former startup was the poster child for Silicon Valley’s time-honored strategy of not letting a balance sheet get in the way of a good story (see: high valuation).

But those days are long gone now that venture capitalists have tightened their purse strings. That’s resulting in a cash crunch for late-stage companies, forcing them to fold or sell off their best assets, writes Insider’s Vishal Persaud.

It’s not just formerly high-flying tech startups, though. Small-business bankruptcy filings are also on the rise, according to The Wall Street Journal.

Of course, you wouldn’t know things are so bad from WeWork’s bankruptcy announcement. The message reads more like a company on the rise than one legally acknowledging it can no longer pay its debts, writes Insider’s Katie Notopoulos.

But maybe there’s a reason for the optimism. There’s a theory making the rounds that WeWork is considering bringing its eccentric confounder and former CEO Adam Neumann back into the fold.

Because if we’ve learned anything from the WeWork debacle, it’s that no one has learned anything.

Moody’s Investors Service lowered its ratings outlook on the United States’ government to negative from stable, pointing to rising risks to the nation’s fiscal strength. The ratings agency has affirmed the long-term issuer and senior unsecured ratings of the U.S. at Aaa.

Moody’s move to cut its outlook arrives as Congress faces the looming threat of a government shutdown once more. The government is funded through next Friday. Newly elected House Speaker Mike Johnson said he plans to release a Republican government funding plan on Saturday.

First Drukenmiller and now Griffin used the term “spending like a drunk sailor”

Since the US Treasury’s $31.4 trillion borrowing limit is suspended until Jan. ‘25 (see below)

And getting re-elected in '24 is Job #1 for the President & everyone trying to return in Congress,

Then I expect the borrowing & spending for eco stimmy to continue.

The centerpiece of the agreement remains a two-year suspension of the debt ceiling, which caps the total amount of money the government is allowed to borrow. Suspending that cap, which is now set at $31.4 trillion, would allow the government to keep borrowing money and pay its bills on time — as long as Congress passes the agreement before June 5, when Treasury has said the United States will run out of cash.

According to Kyle Bass, we’re spending $6 trillion and taking in $4 trillion.

Even drunken sailors have to stop spending when they run out of money

©Copyright 2017 Coogfans.com